Satcom revenues and capacity demand are expected to show significant expansion over the next decade with key growth opportunities arising in universal broadband access, mobility (aero, maritime, land), and defense/security applications. Fixed Satellite Service (FSS) revenues are anticipated to rebound as global satellite capacity supply rapidly increases. In a competitive and increasingly data-focused market, vertical integration is crucial for recouping investments in evolving technology.

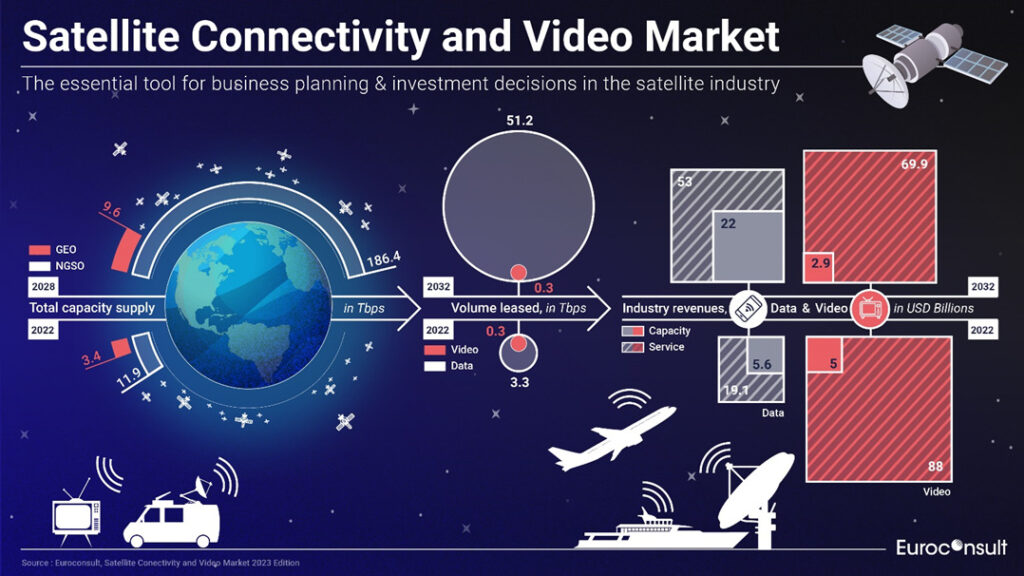

Paris, Washington D.C., Montreal, Yokohama, Sydney, September 25, 2023. The satellite communication landscape is poised for a transformative decade of growth as satellite capacity demand is projected to surge from 3.6 Tbps (TeraBytes Per Second) in 2022 to 51 Tbps in 2032, representing a 31% CAGR (compound annual growth rate), with all data segments expected to observe exponential growth in the next 10 years.

Euroconsult’s latest ‘Satellite Connectivity & Video Market’ market intelligence report unveils three major growth prospects for the satcom industry: universal broadband access, mobility (including aero, maritime, and land mobility), and defense and security applications. Additionally, Satcom service revenues are set to rebound starting in 2023 following several years of negative growth, with revenues predicted to rise from $108 billion in 2023 to $123 billion by 2032, totalling an estimated $1.15 trillion in cumulative revenues over the next decade.

Furthermore, the global satellite capacity supply is on the brink of a dramatic increase, with a 62% rise in 2022 alone, reaching 15 Tbps, primarily driven by Starlink. Anticipated to reach nearly 200 Tbps by 2028, this expansion coincides with the introduction of new non-geostationary orbit (NGSO) constellations, particularly in the low Earth orbit (LEO), including Telesat Lightspeed and Amazon Kuiper, alongside Gen 2 constellations for Starlink and OneWeb, and Very High Throughput Satellite (VHTS) deployments like Viasat-3, Jupiter-3, and Satria-1. Consequently, the share of NGSO in the total supply is forecasted to surge from 76% in 2022 to over 95% post-2026.

“The satcom industry finds itself in a dynamic phase following substantial investments in satellite infrastructure, presenting both fresh opportunities and heightened competition,” said Dimitri Buchs, Managing Consultant at Euroconsult. “The forthcoming wave of new satellite infrastructure will herald a transformative era for satellite operators, necessitating strategies to recoup investments. This entails a focus on vertical integration to optimize costs and scale, coupled with value-added services that enhance proximity to customers and end-users, alongside a concerted drive toward emerging and high-growth market segments.”

In recent years, satellite operators have adapted to the shift from a video-centric market to a more data-focused market, resulting in substantial investments in network expansion and service diversification. Consequently, vertical integration has gained ground in recent years characterized by the acquisition of service providers, satellite manufacturing and investments in user terminals. Market dynamics continue to evolve, with recent months seeing notable consolidations, such as the completion of the Viasat-Inmarsat merger and the Eutelsat-OneWeb merger soon expected to be approved.

New satellite technology is acting as a catalyst for improved economics, including lower capacity pricing and the capacity to provide higher provisioning rates per site and expanding availability of unlimited data plans. These advancements will be pivotal in meeting the burgeoning demand for satellite capacity, particularly in segments like enterprise networks with cloud applications and the largely untapped land mobility market.

Euroconsult is now offering a free extract from the report for download, providing a preview into the key market insights available within the full report.