The Earth Observation (EO) market has undergone shifts in financing, with optical constellation operators going public to accelerate their deployment and to develop new services. Furthermore, the EO market experienced a payload diversification with emerging constellation operators offering new types of data (hyperspectral, infrared, etc.), thus expecting to unlock new markets and value-added services (VAS). Leading global strategists at Euroconsult provide an in-depth analysis of the data and services market in a new edition of their Earth Observation: Data & Services Market report.

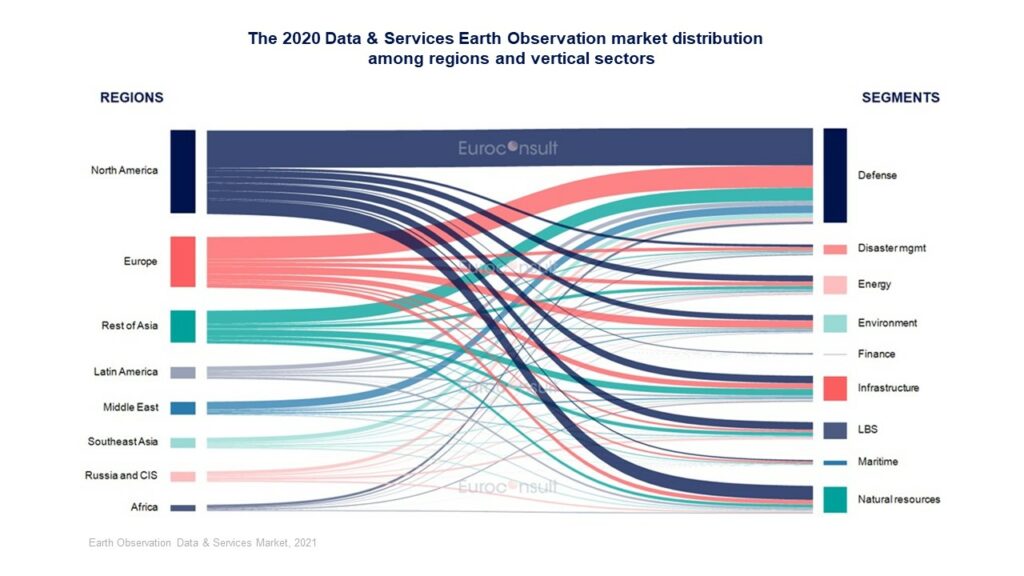

Paris, Washington D.C., Montreal, Yokohama, Sydney, Toulouse, 6, October 2021 – Euroconsult has released its latest Earth Observation: Data & Services Market (EODSM) report for 2021, providing a fresh global assessment of the Earth Observation (EO) satellite-based commercial demand for imagery and value-added services, in 8 regions and across 9 vertical markets.

In 2020, the commercial market for EO data stood at $1.6 billion, growing at a 5-year Compound Annual Growth Rate (CAGR) of 5%. It is expected to top $2.5 billion by 2030 at 4% CAGR throughout the decade. In its comprehensive overview of the EO market, EODSM 2021 observes that defense maintains its place as the most significant market for commercial data & services, with $1.8 billion in 2020, or around 45% of the total market.

The Value-Added Services market is also expected to undergo an accelerated growth driven by constellation supply, topping $5 billion by 2030 with 7% CAGR through the decade. Still fragmented, some emerging but promising applications such as LBS and insurance are expected to lead the growth due to the increasing bigdata and data fusion capabilities.

The report also gives a comprehensive overview of major events occurred last year with a unprecedent impact in Earth Observation sector such as:

- The first slow-down in EO fundraisings in 2020 due to covid crisis which favored Series B and C of the most advanced operators.

- An unprecedented rebound with billions raised during SPACs of leading constellation operators in 2021, expected to trigger many mergers & acquisitions in the next few months.

- A new record in EO satellites launched due to the emergence of large rideshares of SpaceX, making constellation deployments and renewals faster.

- The first constellations reaching full operational capabilities, expecting to unlock new markets based on high revisit change detection services.

- A strong diversification of miniaturized payloads embedded in constellations with the emergence of first commercial hyperspectral and infrared capabilities.

As every year, the data and VAS model have been refined according to interviews of leading operators. Furthermore, the refinement got benefits from revenues publications of an increased number of listed operators which went public (Special Purpose Acquisition Company (SPAC), traditional IPO, or company transfer), thus providing a finer estimate of the EO market by resolutions.

In particular, the report has a look at revenues by type of resolutions for multispectral imagery, considering now revenues from both incumbent and constellations operators of optical sensors, considering the maturation of the market. A shift in supply disrupts the 0.5-1m resolution market, as well as coarser resolutions with a wide range of constellation projects. Conversely, EODSM 2021 is still observing a race to the most resolute, now commercially reaching less than 30cm, with Airbus and Maxar leading the optical scene and ICEYE, Capella, and Umbra in the Synthetic Aperture Radar (SAR) scene, all targeting the defense market.

Brand new to the 2021 edition, the report also highlights the growing influence that the development of new types of data. Indeed, EODSM 2021 now features demand analysis by sensors that include benchmark and roadmap for Multispectral-VNIR, Hyperspectral & Multispectral-SWIR/MWIR/LWIR as well as SAR domains by sectors.

Indeed, more affordable satellite constellations have created an opportunity for specialized sensors to meet the requirements of a growing user base. These new sensors are expected to leverage open-source data from Copernicus & Landsat programs to bring a higher revisit and thus unlocking new markets with new services ranging from vegetation water stress detection to wildfire anticipation.

Subscribers to the Premium Edition will be granted full access to a complete database of the market by sensor types with details by main resolution, the service market and the distribution by the 9 sectors for each category of sensors, a complete database of the Earth Observation private equity funds raised by companies from 2011 to 2020, as well as an extension of the report with 25 pages profiling 14 leading operators, 27 new commercial operators and a sample of pure value-added service providers specialized in Artificial Intelligence processing.

The 14th edition of Euroconsult’s Earth Observation: Data & Services Market is available for purchase now on their Digital Platform and is an essential tool for gaining a complete understanding of the current earth observation market.