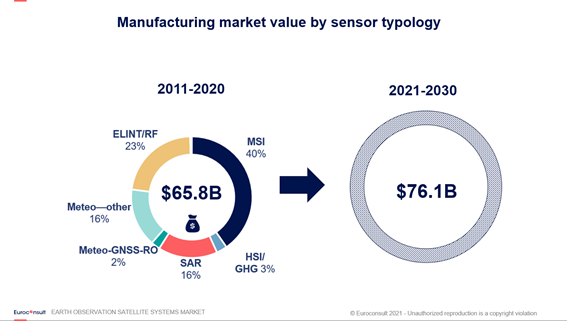

The advent of commercial satellite constellations has led to satellite platform miniaturization and a strong diversification of commercial payloads, in particular with SAR, Hyperspectral, ELINT/RF and GNSS-RO. While most of the 2,600 satellites to be launched in number will be commercial ones, the bulk of the generated $65.8 billion in manufacturing revenues between 2011-2020 will keep being driven by civil and military government programs over the next decade to reach $76.1 billion by 2030.

Paris, Washington D.C., Montreal, Yokohama, Sydney, Toulouse, January 13, 2022 – Euroconsult, the leading space consulting and market intelligence firm, has released its eagerly awaited ”Earth Observation Satellite Systems Market” report, providing a sweeping review analysis of the Earth Observation (EO) upstream ecosystem and breaking down government and commercial programs in exhaustive details. With the Earth Observation manufacturing market gearing up for another decade of growth to an estimated $76.1 billion in revenue, the latest study reflects profound changes in the market structure driven by the diversification of payloads and multiplication of commercial constellation projects.

Over 2011-2020, the commercial satellite constellations accounted for 65% of EO satellite launches but captured a negligible 4% of the market value, as opposed to government-funded programs which secured over 80% of satellite value. This discrepancy between volume and value is a salient result of the boom in commercial constellations, turning to Commercial-off-the-shelf components and low CAPEX per satellite business models. This trend is projected to be further ingrained over the next decade, growing from 1,080 launches between 2011 and 2020 to no less than 2,600 by 2030, with as many as 90 constellations accounting for 78% of EO satellites to be built and launched.

On the other hand, government programs remain the principal value creator on the market, generating $11.8 billion in manufacturing revenue in 2021 (excluding ELINT/RF), with civilian programs seeing the 14th consecutive year of growth. With both private and public stakeholders on a growth trajectory in this new structure, manufacturing revenues are expected to follow suit with government R&D and commercial portfolio diversification as the main drivers.

One of many major insights from this year’s report is the diversification of investments beyond optical-multispectral payloads, signaling another step towards market maturity and echoing the development of commercial constellations. Of particular significance is a surge in investment into commercial satellite constellations precipitated by the diversification of missions towards HSI, SAR, ELINT/RF, GhG, GNSS-RO.

The ”Earth Observation Satellite Systems Market” offers the most specialized and detailed breakdown of the Earth Observation upstream market available today. Designed to help stakeholders navigate evolving market dynamics with actionable insights, this report paints a comprehensive picture of technological and policy drivers with benchmarking for manufacturers and payloads, policy and regulation overviews for the upstream value chain, as well as demand dynamics analysis across commercial and governmental markets, including civilian applications and declassified defense projects.

At the turn of a new decade, this year’s edition of the report launches with an updated outlook on the next 10 years of the EO manufacturing market, featuring an exhaustive database of both satellites launched and of those to be built and launched. This industry-leading data is put into perspective with an updated satellite systems demand dynamics forecast to 2030, broken down by region, satellite owners, manufacturers and launch providers and cross-referenced with payload typology and mass category.

Premium customers will enjoy access to even more expansive analysis from Euroconsult’s digital platform and benefit from powerful tools to effortlessly review and conveniently visualize and export relevant data. In addition to features listed above, the Premium edition boasts an exclusive look at a complete EO procurement index with a global map outlining the positioning of countries for future EO purchases, as well as a supplemental 23 pages of analysis of the global EO landscape for every country. Finally, the exhaustive satellite database is available with additive information such as the EO mission type, GSD and Dual-use typology. The 2nd consecutive year release and the 14th edition as part of the famous ”Earth Observation Satellite Systems Market” is the definitive tool for satellite manufacturers, operators and investors and both Classic and Premium versions are available now on Euroconsult’s digital platform: https://digital-platform.euroconsult-ec.com/product/earth-observation-satellite-systems-market/