The latest edition of Euroconsult’s “High Throughput Satellites” report investigates the effects of recent constellation developments on HTS production and market, as well as the long-term impact on global communications.

Paris, Washington, Montreal, Yokohama, Sydney, Toulouse, March 23, 2022 —Euroconsult has released the 6th edition of its High Throughput Satellites (HTS) report – its in-depth analysis of geostationary (GEO) and non-geostationary (NGSO) HTS markets including major drivers, strategic issues, competitive landscape and detailed forecasts of capacity supply and associated demand take-up.

After helping reshape the satellite communications industry through their ever-improving capacity volumes and cost per bit, High Throughput Satellites are entering a new era of accelerated and drastic transformation, wherein global HTS capacity supply is expected to grow at a torrid pace over the next five years (45% CAGR) surpassing 60,000 Gbps (60 Tbps).

Facilitating this growth are non-geostationary orbit (NGSO) broadband constellations, which are projected to account for nearly 90% of capacity supply in 2026, a marked contrast to the historically dominant market share of supply held by GEO-HTS systems.

Recent NGSO momentum has been underpinned by the aggressive launch campaign of SpaceX’s Starlink LEO constellation, which nearly single-handedly led to a 350% expansion of global HTS capacity supply in 2021 alone after entering initial operational status. While other NGSO constellations have faced a mix of development and launch delays, OneWeb and SES (O3b mPOWER) are poised to enter initial service in 2022.

Euroconsult notes that NGSO supply figures, despite being adjusted to reflect sellable capacity (as opposed to notional aggregate constellation capacity), must be treated with caution as not all projected capacity can be immediately exploited due to lagging national market access authorizations and gradual gateway deployments.

Faced with the on-going shift in capital towards NGSO broadband constellations, the GEO-HTS segment will continue its growth, albeit at a more moderate pace. In response to market uncertainty caused in part by NGSO and large-scale GEO-VHTS systems such as Viasat-3 and Eutelsat Konnect, GEO-HTS operators have responded by adopting software-defined satellite architectures to help reduce market risk and improve agility. Fully software-defined satellite platforms from manufacturers such as Airbus, Thales and new entrant Astranis have accounted for over 50% of GEO-HTS orders over the 2019-21 period and more than 80% of GEO-HTS orders in 2021 alone.

“High throughput satellite technology has never been better positioned to help bridge the rural digital divide through a combination of innovation and scale, notably through NGSO (non-geostationary) constellation architectures,” said Brent Prokosh, Senior Affiliate Consultant at Euroconsult. “This in turn will drive significant improvements in value and performance of satellite broadband services”.

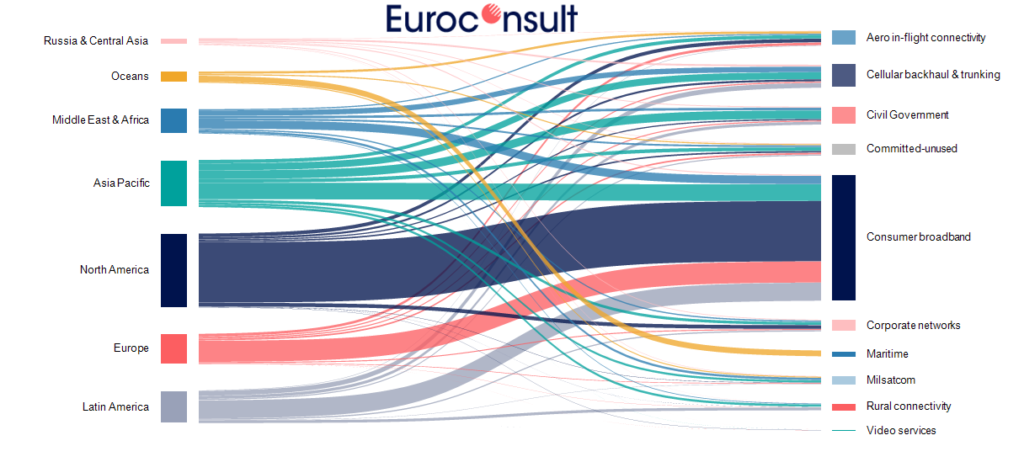

Overall, Euroconsult’s comprehensive analysis suggests that business is booming for HTS. Global capacity demand projected to average 28% on a compound annual basis through 2030, with the consumer broadband segment poised to account for nearly 60% of net capacity growth globally. Next-generation HTS technology is driving material improvements to the performance and value of satellite broadband offerings that will not only disrupt legacy satellite services, but expand the addressable market for HTS by improving competitiveness against rural terrestrial alternatives such as mobile hotspots and ageing DSL infrastructure.

From a regional perspective, Euroconsult expects that HTS demand growth will be spread more evenly rather than the more concentrated and localized historical expansion, notably due to the ubiquitous nature of NGSO constellations which serve all regions. For example, North America, which accounts for 50% of HTS capacity demand as of 2021, is projected to account for just 33% of global demand by 2030.

Interestingly, the report also highlights that due to falling capacity pricing, the total HTS capacity revenue, while still significant, is projected to be lower than demand growth. Operators are therefore moving towards end user services as a means to combat expectations of intensifying pricing pressure in wholesale leasing markets.

About The Report

“High Throughput Satellites: Vertical Market Analysis & Forecasts” provides both quantitative and qualitative assessments of the growing market and strategic landscape. It is an essential tool for satellite and telecommunications executives, companies competing in the HTS markets, as well as investors in both upstream and downstream services.

To keep pace with this evolving market, Euroconsult has for the first time introduced a quarterly update on NGSO constellations which tracks progress in the space segment, ground segment and commercial and market developments for each of the main operators, as part of its Premium subscription service.

“This report comes at an opportune time as HTS platforms are poised to be by far the leading type of space infrastructure from the perspective of commercial growth potential over the next 10 years with wholesale capacity revenues projected to top $100 billion in aggregate from 2021-30”, said Prokosh.

It is available now and can be ordered from the Euroconsult shop.